As the adoption of electric vehicles grows, the demand for efficient and widespread EV charging infrastructure is increasing. Key areas include:

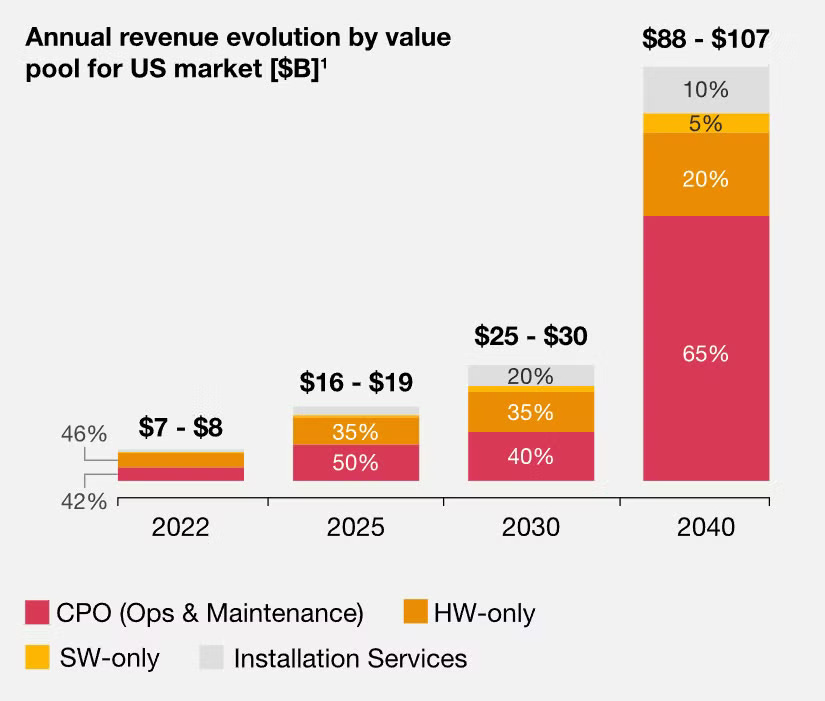

Figure 19: US EV infrastructure revenue projection [16]

The US electric vehicle (EV) infrastructure market is anticipated to expand significantly, reaching approximately $100 billion by the year 2040. Charge Point Operators (CPOs) are expected to generate the majority of revenue within the Electric Vehicle Supply Equipment (EVSE) sector through comprehensive turn-key solutions. Revenue from advanced hardware solutions, essential for bi-directional charging and sophisticated home energy systems, is projected to contribute around $20 billion. While software plays a crucial role in enabling CPO solutions, the direct revenue from software alone is expected to represent only a small fraction of the total market.

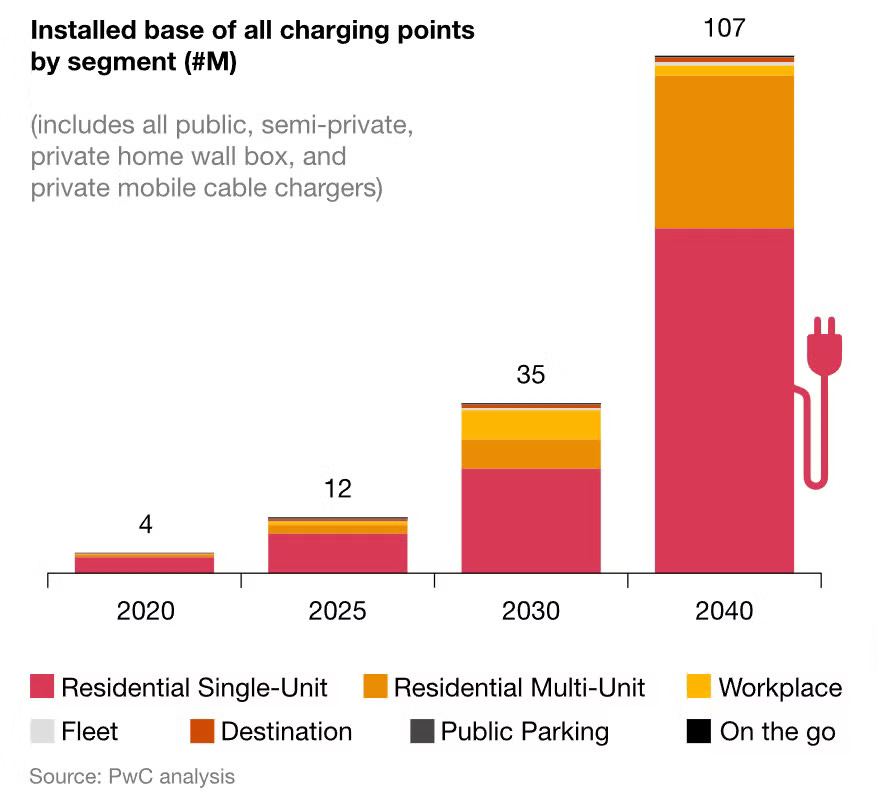

Figure 20: EV charging point by segment [16]

According to recent PWC studies, the workplace charging segment is projected to experience rapid growth, expanding from virtually nonexistent to approximately 17% of the market, translating to about 6 million charging points by 2030. Similarly, charging infrastructure in apartment buildings, or multi-unit residential settings, is expected to see significant growth. Starting from almost zero, it's anticipated to capture about 15% of the market by 2025 and further increase to 17% by 2030.

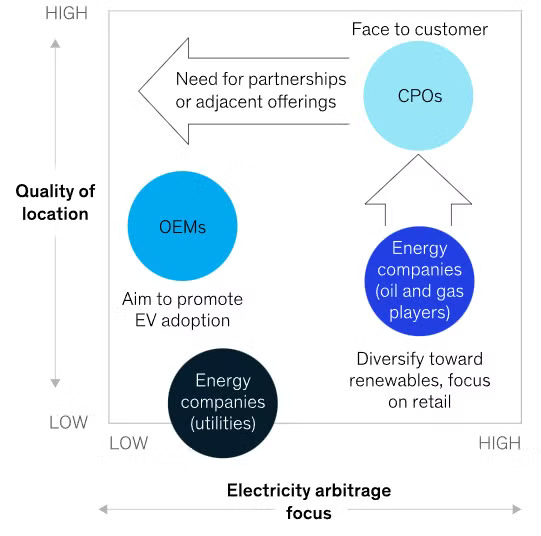

Figure 21: EV charging station market ecosystem [17]

The electric vehicle charging infrastructure (EVCI) landscape is shaped by various strategic approaches:

{kind=link}

{kind=link}

{kind=link}